Last updated: 6 Sep 2024

Extended home building manifesto

Home building: An engine for growth, prosperity and opportunity

Explore the recommendations of our housing blueprint in more detail and how industry's recommendations be best implemented by the new government.

Please note: This is an extended version of our housing blueprint - Home building: An engine for growth, prosperity and opportunity - published June 2024.

Contents

- Introduction

- Housing delivery is in freefall

- Home building is facing a watershed moment: Reasons for the decline in housing delivery

- HBF’s blueprint for a brighter future

- Housing the nation: Homes to meet the needs of the country

- Increasing housing supply: Establishing a clearer and more certain policy landscape

- Fixing the planning process: Tackling systemic issues hindering delivery

- Unblocking the housing pipeline: Finding a resolution to nutrient neutrality

- Greener growth: Building blocks for high quality, green homes

- Contact details

Download Home Building: An Engine for Growth, Prosperity and Opportunity - Extended version in full.

Introduction

The home building industry is at the coalface of tackling the housing crisis. Over the past five years alone, it has delivered around 1.2 million much needed new homes, helped hundreds of thousands of people realise their home ownership aspirations, and provided half of all Affordable Housing.

However, the contribution industry makes stretches far beyond just bricks and mortar. Each year, home building:

- supports around 750,000 jobs and over 8,000 apprenticeship positions.

- generates over £40bn in economic activity.

- contributes more than £70 million for open spaces.

- provides almost £195m for the development of new and existing schools.

- enables £12.5bn spending in supply chains and £6.3bn spending in local shops.

If housing delivery were to increase, this would not only provide vital new additions to this country’s housing stock but deliver further significant benefits for both the economy and local communities. Indeed, it is estimated that every 100,000 new homes built adds 1% to GDP.

Housing delivery is in freefall

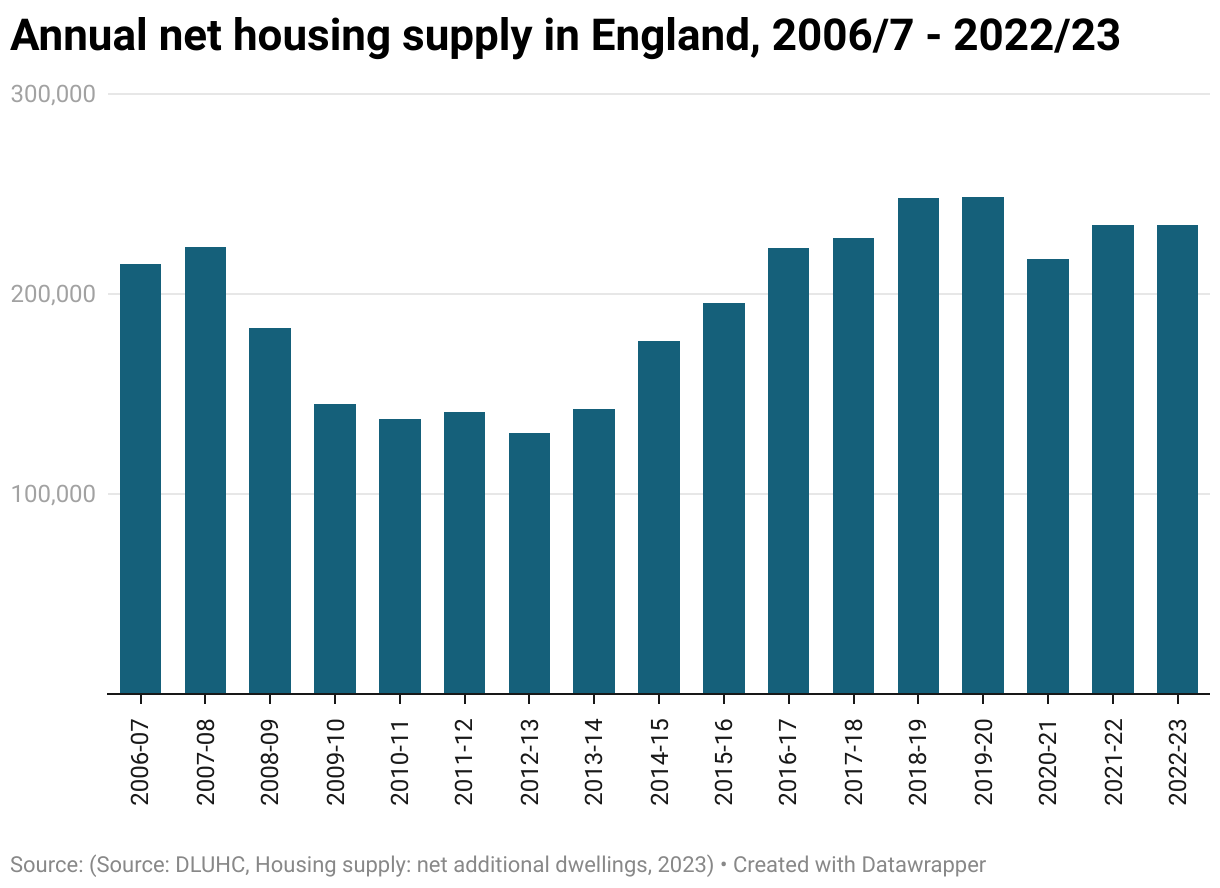

While industry built more than 234,000 new homes in 2022-23, delivery remains considerably lower than the number of homes needed.

Due to decades of undersupply, England has far fewer dwellings relative to its population than other developed nations we typically consider peers, with 434 homes per thousand inhabitants, significantly fewer than France (590), Italy (587) and the OECD average of 487.

For England to ‘catch up’, a record-breaking net supply of 320,000 homes per year – nearly 100,000 more than current delivery levels – would be required.

However, with all available metrics suggesting that in the coming months and years house building is set to decrease, it remains an ambition that is moving ever further away:

- Falling planning permissions – HBF’s Housing Pipeline report found the number of units achieving planning permission in the year ending Q1 2024 was 236,644 - the lowest 12-month total for almost a decade, since Q3 2014. Year on year, this is a 13% drop, and 22% on the year to Q1 2022. Furthermore, the number of units approved during Q1 2024 – 53,862 – is the lowest quarterly total since Q2 2015. This is a 19% drop on the previous quarter and 13% on the same period last year.

- Some regions are faring worse than others. London, where affordability and availability are already the most stretched, saw a 39% drop year on year and a 51% drop on the previous quarter.

- In England, the number of sites granted permission in Q1 2024 – 2,472 – was the lowest quarterly figure since the HBF Housing Pipeline Report began in 2006 – a 10% drop on the previous quarter. This is around half of the number of sites that were being approved in the latter half of the 2010s, when housing supply was at its peak.

- Reduction in EPCs issued - One measure of recent completions, the number of new homes issued with an Energy Performance Certificate, shows a 6% fall in new build completions for the 12 months to March 2024 compared with the equivalent period a year earlier.

- Additions to the Council Taxbase in the year to September 2023, showing the creation of new addresses, saw a fall in recent years.

- uid

- None

- ctype

- None

- heading

- None

- content

Home building is facing a watershed moment Reasons for the decline in housing delivery

The reasons for the decline in housing delivery are vast, including, but not limited to:

- Paralysis in the planning process: Underfunded and under resourced Local Planning Authorities (LPAs), the complexity of the planning process and the lack of timely responses from statutory consultees are resulting in increased delays, uncertainty and costs for developers of all sizes, across the country. The recent Competition and Markets Authority (CMA) house building market study report found that only 12% of planning applications were determined within 13 weeks and the direct costs associated with making planning applications can range from £100,000 to £900,000 depending on the site.

- SME home builders are in decline: While all developers face challenges with planning, SME developers experience them most acutely by virtue of their size. In addition, they are also struggling with land availability, due to the lack of small sites that are being brought forward through Local Plans.

- Nutrient neutrality mitigation requirements: At least 160,000 new homes remain blocked by Natural England’s moratorium on house building in 74 local authorities despite evidence that the occupants of new homes contribute less than 1% to the problem of nutrient pollution in rivers.

- Abolition of mandatory housing targets: Research by Lichfields for HBF shows that recent changes to the NPPF could result in a drop of 77,000 homes a year. Despite only being confirmed in December 2023, the policy has already had a negative impact on housing delivery with more than 60 Local Authorities either pausing work on or withdrawing their local plans since the announcement was made.

- Lack of support for first-time buyers (FTBs): Builders can only build if buyers can buy and that has become increasingly difficult, particularly for FTBs, due to the economic climate, higher interest rates and the closure of the Help to Buy Equity Loan Scheme (HtB) in March 2023. The closure of the scheme left aspiring owners without any form of Government support scheme for the first time in over 25 years.

- Uncontracted s106 Units: A recent survey of a small selection of HBF members found that there are at least 13,000 Affordable Housing units with detailed planning consent that remain uncontracted with Registered Providers (RPs). This is due to a ‘perfect storm’ of financial pressures faced by RPs, resulting in a prioritisation of grant funded properties.

As a result, the election of a new government presents a real watershed moment for the industry in terms of future housing policy and its impact on supply.

- uid

- None

- ctype

- None

- heading

- None

- content

HBF's blueprint for a brighter future

Home builders want nothing more than to tackle the housing crisis, build vibrant new communities and for industry to play its part in increasing the growth, prosperity and opportunities of the country.

For industry to achieve its potential, a constructive and collaborative partnership between home builders and the new Government will be needed, alongside a pragmatic and evidence-based approach to policy making.

HBF recently published a blueprint of policies, Home building: An engine for growth, prosperity and opportunity, which outlines the actions industry considers would support not only the delivery of new homes but economic growth.

The remainder of this paper explores these recommendations in more detail and sets out how they could be best implemented by the next government.

- uid

- None

- ctype

- None

- heading

- None

- content

Housing the nation: Homes to meet the needs of the country

England is the most difficult place in the developed world to find a home due to decades of under delivery. Not only are people grappling with the poor availability of appropriate housing, this country’s existing housing stock is also:

- Unaffordable - The UK is home to the second most people living in households that are paying more than 40% of their income on housing in Europe. In 2018, the year for which the latest data is available, this stood at 10 million people - 15.1% of the UK population. This proportion is 4.8 percentage points higher than the EU average of 10.3%.

- Ageing - The UK has amongst the oldest housing in Europe, with 78% of homes having been built before 1980, compared with an EU average of 61%, and 38% of the UK’s housing stock being built before 1946, compared with an EU average of 18%.

- In poor condition - 15% of English homes failed to meet the Decent Homes Standard in 2020. This is the highest proportion of substandard homes in Europe, and significantly higher than many other countries including Germany (12%), Bulgaria (11%), Lithuania (11%) and Poland (6%).

This country’s continuous failure to build enough homes is not unique to any tenure and is having a significant impact on all people searching for a home:

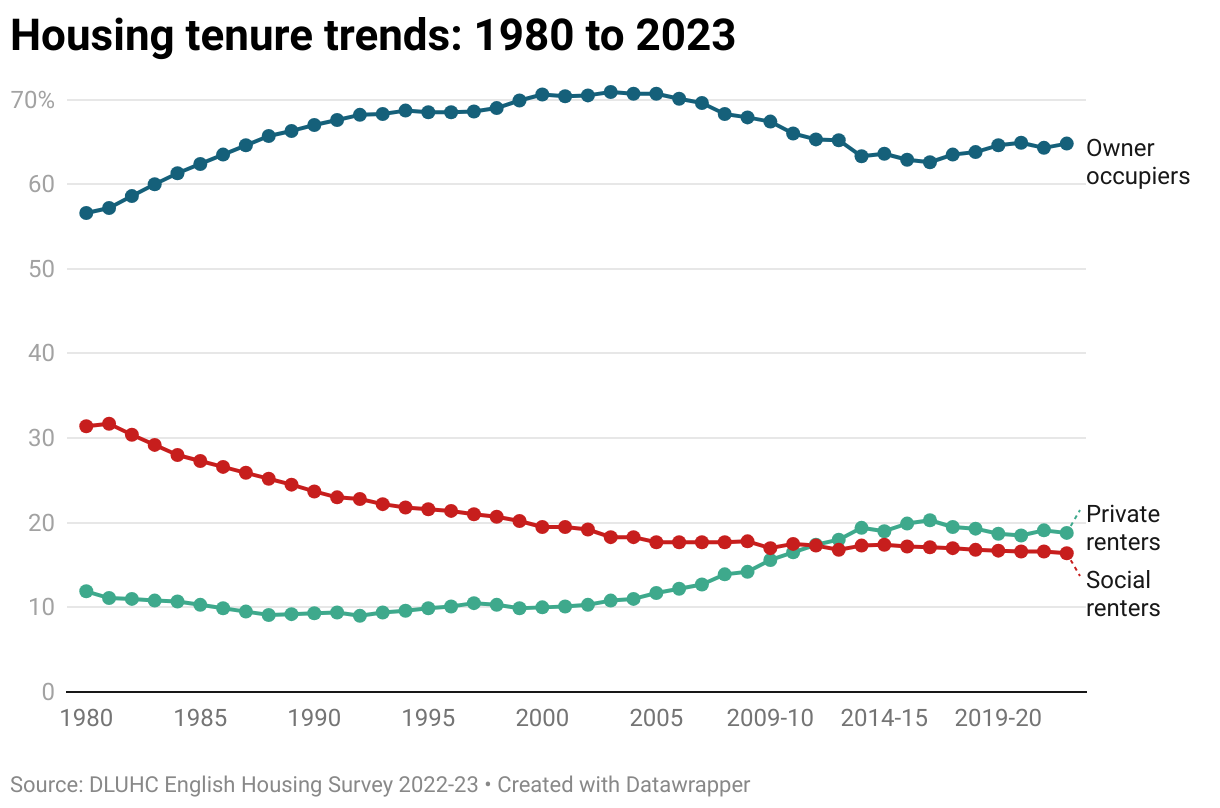

- Home ownership - Home ownership is still the largest tenure but is far lower than its 2003 peak. In2022-23, 64.8% of people were owner occupiers, compared to 70.9% in 2003.

- Private rented sector – An imbalance between supply and demand has seen renters facing record prices with rents growing at the fastest annual rate for more than a decade. Average rents increased to £1,293 a month in England, £730 in Wales and £952 in Scotland in the year up to April 2024.

- Social housing - The social housing sector has shrunk. In 1979, local authorities and housing associations let 5.5 million homes. This number declined by around a quarter over the next 40 years, reaching 4.1 million in 2022. It is estimated that the number of homes forsocial rent fell from 4.0 million in March 2013 to around 3.8 million in March 2023. Meanwhile, local authorities' waiting lists continue to grow; there were 1.21 million households on local authority waiting lists on 31 March 2022, an increase of 2% from 1.19 million in 2020/21.

- Older person’s housing - Research from the Homes for Later Living Group suggests that approximately 25% of the country’s 65+ population (nearly 3 million people) want to downsize. However, there are not enough suitable properties to enable this to happen. It is estimated that we need to build approximately 30,000 properties for later living each year to keep pace with the ageing population.

The remainder of this section will explore these issues in more detail and outline the recommendations HBF would encourage the next Government to introduce to tackle these challenges – as well as how these recommendations could be implemented.

Problem: First-time buyers are finding it increasingly difficult to get on the housing ladder

In England, home ownership is the largest tenure and has been since the mid-1970s. The 2022-23 English Housing Survey found that 64.8% of people were owner occupiers, which is considerably lower than the 2003 peak of 70% (as demonstrated by the chart below).

There are also other causes for concern, with younger generations struggling to access the housing market without the support of family wealth. As home ownership has become less accessible, and following an extended period of low mortgage rates now passing into history, a growing proportion of mostly older home owners are now mortgage-free, again threatening to widen the gap between the haves and have nots.

Housing wealth is becoming increasingly entrenched

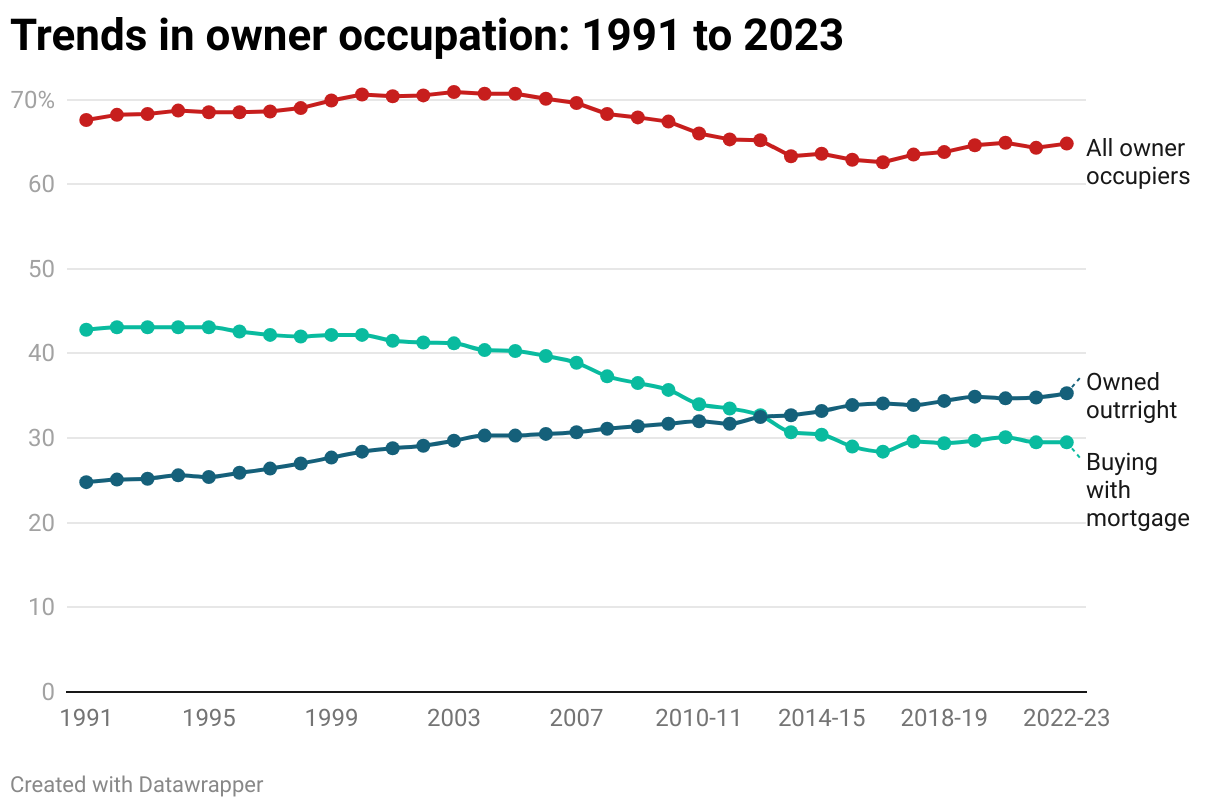

In 1991, 24.8% of homeowners were outright owners. By 2022-23, this had increased by over 10 percentage points to 35.3%. Meanwhile, those buying a home with a mortgage fell from 43.1% in the early to mid-1990s to 29.5% in 2022-23.

Housing affordability has worsened considerably in England over the past 20+ years

Full-time employees in England could expect to spend around 5.1 times their workplace-based annual earnings on purchasing a home in 2002. By 2022, this had increased to 8.3.

Younger people are far less likely to be home owners than they were almost 20 years ago

In 2004, 56.7% of people aged 25-34 were owner-occupiers. In 2022-23, the figure was just 44.7% and has been below 50% every year since 2009-10.

The average age of first-time buyers is increasing

From 31.4 in 2003-04 to 33.5 in 2022-23.

The majority of recent first-time buyers are from the two highest income quintiles

In 2022-23, 58% of FTBs were among the highest earners.

Nearly half of first-time buyers rely on friends or family for their deposit

In 2022-23, 45% of FTBs used either inheritance or a gift or loan from loved ones for their deposit, up from 36% in 2015-16.

The current situation for FTBs is particularly challenging due to the closure of the Help to Buy Equity Loan scheme in 2023, which supported almost 400,000 buyers into home ownership during its lifetime and as of March 2023 had delivered £700 million in returns to the Exchequer from repaid equity loans.

Indeed, it is the first time in over 25 years that there has not been a government support scheme in place to support aspiring homeowners, and at a time when it has arguably never been needed more.

Solution: Introduce a new, targeted home ownership scheme for first-time buyers (FTBs) who want to buy a new, energy efficient property.

Any solution aimed at helping FTBs on to the property market needs to tackle two main barriers to be successful.

The first key challenge is the amount required for a deposit, with the average (mean) deposit of a first-time buyer in 2022-23 reaching £50,000 (£30,000 median).

Mortgage affordability is the other. Earlier this year, HBF research, based on the average purchase price for first-time buyers (FTBs), over the past 24 months, found they had experienced a 220% increase in annual mortgage payments.

While inflation (and interest rates) looks to be heading in the right direction, the days of historically low interest rates are seemingly behind us. The solution, therefore, must address both of the issues to help as many FTBs into ownership as possible.

To that end, HBF would welcome the introduction of a new equity loan scheme, targeted at aspiring home owners. A new scheme would:

- boost first-time buyers’ deposits, giving them access to new build mortgages which are priced more affordably

- see developers paying a fee similar to the ‘commercial fee’ payable by mortgage lenders for access to the Mortgage Guarantee Scheme

- involve developers covering a portion of the upfront investment in the form of a fee which would see HMG retain the full equity share.

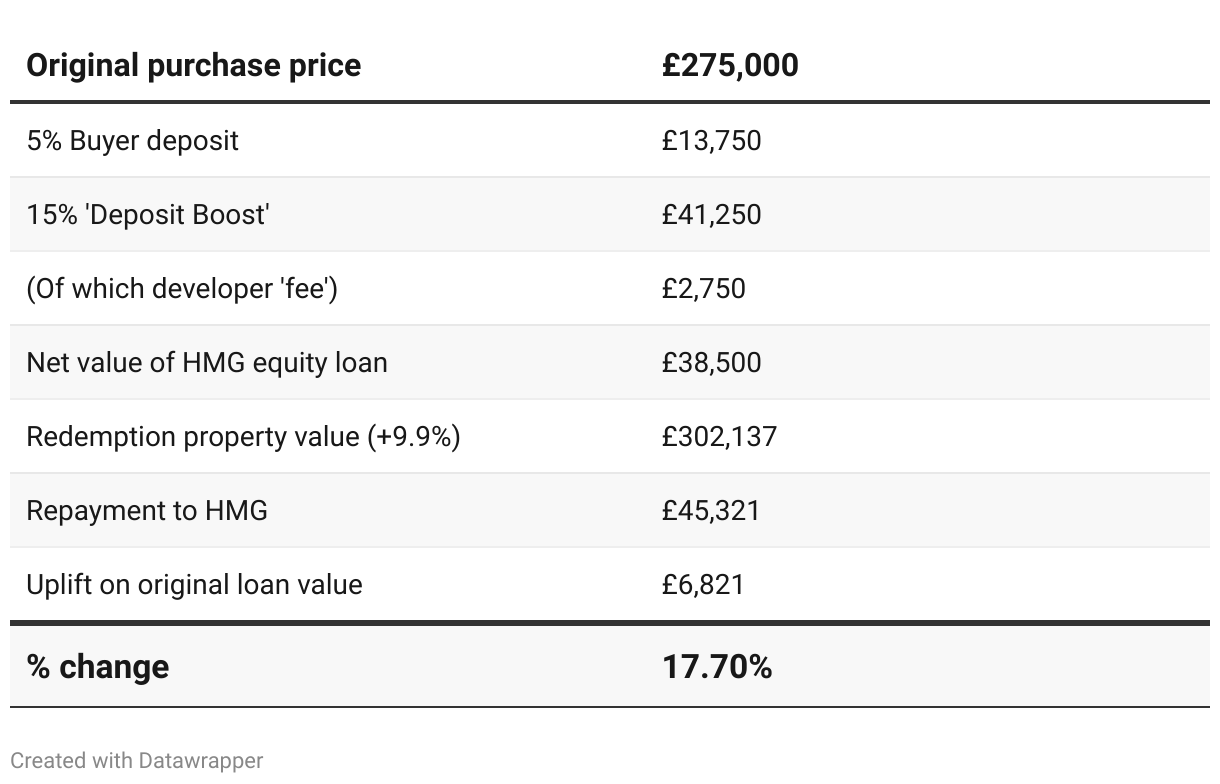

Under this proposed scheme, FTBs would require a 5% deposit. This would be matched in the form of a 15% equity loan from Government, which would include a developer fee from the participating developer, equivalent to 1% of the sales price.

As a result, home buyers would gain access to a greater range of mortgage deals at far lower rates. 80% Loan to Value (LTV) mortgages are priced significantly cheaper than those above this level because of mortgage regulations governing capital requirements on LTV lending and risk weightings applied to portions of lending above 80%. By providing a government equity loan of 15% and reducing the LTV to 80%, buyers are more likely to benefit by falling below 4.5x Loan-to-Income ratios and thus, again, having access to more mortgage deals and cheaper pricing.

A homebuyer purchasing a £275,000 new, energy efficient home using a 5% deposit (£13,750) would be able to access a new build mortgage and would see monthly repayments reduced from around £1,450 to approximately £900.

Because the developer will not retain an equity stake, house price inflation benefits would be taken only by the homeowner and the Exchequer.

Supporting around 20,000 transactions per year (split 85/15 outside London/in London) would require the origination of equity loans worth £900m per year, of which more than £60m would be covered by developer fees. This £840m net initial support from HMG is less than half of the current Help to Buy annual income secured through redemptions and interest payments.

Worked example

First-time buyer purchasing a £275,000 property:

- 5% buyer’s deposit (£13,750)

- 15% Government ‘deposit boost’ equity loan (£41,250), of which:

- 14% from Government (£38,500)

- 1% from developer (£2,750)

When the equity loan is paid off, Government would receive 15% of the value of the property despite the net upfront contribution having been 14% of the property value at origination. This is assuming that after three or five years, before interest is payable, the homeowner remortgages and repays the equity loan. This is the typical experience with Help to Buy. Should the value of the property have increased by 10% to £302,000 (1.9% compound HPI per annum assuming a five-year interest free period), the buyer repays Government £45,321.

Consideration could be given to the requirement for all homes purchased to be Energy Performance Certificate rated A-B – which are significantly cheaper to run and so more affordable for those purchasing them.

With regards to the potential for the introduction of price caps, Help to Buy regional price caps set in 2018 have suppressed first-time buyer opportunities in the north of England. As an alternative, a simple price cap structure of £600k in London and £450k elsewhere would mirror other schemes and provide simplicity for buyers. For London, consideration could also be given to a higher maximum equity loan amount. This could be 20% rather than the 15% elsewhere, reflecting constrained affordability and higher prices.

Solution: Make home ownership a reality for more people through the expansion of green mortgages, whereby the savings that energy efficient homes can offer on utility bills are factored into mortgage affordability criteria.

There are a number of measures beyond the introduction of a new first-time buyer support scheme that could help make home ownership a more affordable prospect while helping the country deliver on its environmental goals.

Despite the energy efficiency benefits new build homes provide, consumers are often unable to reap the full financial benefits of choosing a more energy efficient property. While mortgage providers frequently market “green mortgages”, these often see homebuyers benefit from a one-off cashback payment of a few hundred pounds. Therefore, although welcome, in practice they amount to more of a marketing tool rather than a proper green incentive for consumers.

HBF considers that buyers should benefit from the financial and environmental savings that the most energy efficient homes can offer, and that the actual running costs of the property being purchased should be factored into mortgage affordability calculations.

To put the scale of the potential savings into context, the average new build home is powered by 57% less energy, cutting energy bills by up to £183 a month. That's an annual saving of almost £2,200 on new build houses.

Despite the considerable differentials in the cost of heating new build homes compared with older properties, and the increasing percentage of monthly running costs that energy bills now represent, most mortgage affordability calculations include a single national average energy bill across all types of home regardless of the property’s efficiency.

The mortgage lending industry is effectively incentivising consumers through cheaper mortgage finance and higher loan-to-values to purchase older, inefficient homes which will see home owners face significantly higher long-term costs for maintenance, heating and, potentially, retrofitting.

In a modern market economy, customers should be assessed against the actual expected running costs of the property they will be purchasing rather than a national average energy bill. This would incentivise homebuyers to make eco-conscious decisions and ultimately lead to energy efficiency becoming a more important factor in determining a property’s value.

We would encourage the next Government to facilitate a discussion between industry and the mortgage lenders to explore how this can be taken forward in a more uniform way across the finance sector.

Solution: Encourage the purchase of more energy efficient homes by abolishing stamp duty for purchasers of all homes with an EPC rating of B or above.

Beyond FTBs, there is a need to get the entire property market moving and find additional ways of incentivising people to make energy efficient choices when it comes to their housing.

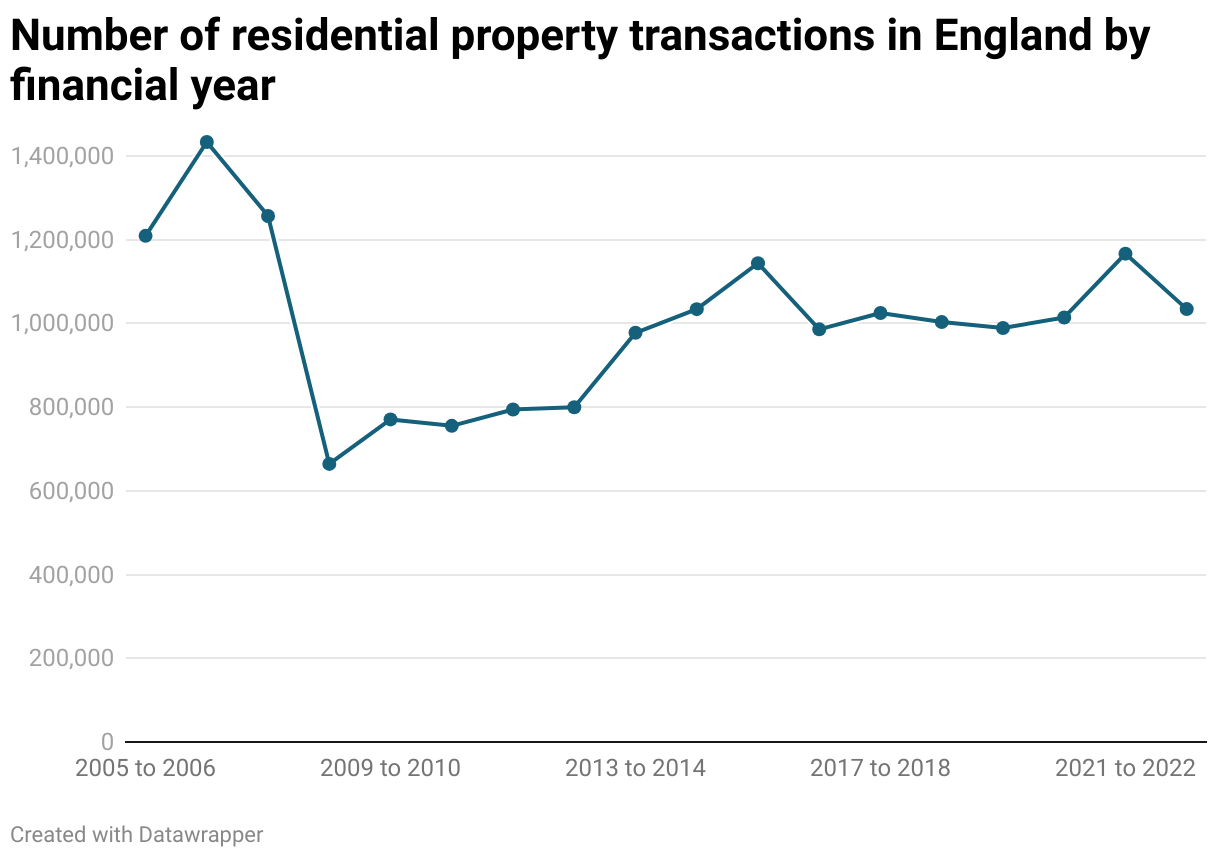

Overall, housing transactions in recent years have been lower than the numbers seen during the 1990s and 2000s. In that period, typically 6-8% of the housing stock would change hands each year. Since 2008, this rate has hovered around 4%.

Inevitably, the uncertain economic environment of recent years has caused the housing market to stagnate further with housing transactions declining rapidly. The total number of residential property transactions in England declined by 11.4% between 2021/22 and 2022/23.

While there are now signs that transaction numbers are on the up once again with April 2024 marking the fourth consecutive month-on-month increase, there is still a long way to go before transaction levels get anywhere close to their peak ( HMRC, UK monthly property transactions commentary, 31 May 2024).

Reversing this shift in housing market activity would be beneficial for the overall market, and the economy more generally. Indeed, HBF/Knight Frank research found that for every 100,000 housing transactions, there is a net impact just shy of £1bn.

To boost housing market activity, Government could look again at its Stamp Duty Land Tax (SDLT) policy. In this respect, research by the London School of Economics found that “the academic literature presents a near-universal consensus that stamp duty is a bad tax. There are three main reasons: first, it reduces mobility which means that the housing stock is inefficiently used: in particular, it reduces the incentive to older households to downsize which leaves younger family households with restricted choices. Secondly, it reduces productivity as people have less incentive to move house to take on a better job. Third, fewer moves mean commensurately lower consumption related to moving, which impacts negatively on economic activity”.

Should the next Government wish to consider some form of action on SDLT, it would be helpful for it to encourage consumers to prioritise energy efficiency by abolishing stamp duty for all purchases of all homes with an EPC rating of B or above.

Problem: There is an ageing population and an inadequate supply of older people’s housing

The number of older people living in the UK is increasing rapidly. The results of the 2021 Census found that over 11 million people – 18.6% of the total population – were aged 65 years or older, compared with 16.4% at the time of the previous census in 2011.

In ten years’ time, this figure is expected to have increased to 13 million or 22% of the population, and by 2032 there will be five million people over 80 living in the UK. However, as the number of older people in the UK increases, the availability of homes specifically designed for later living is failing to keep pace. 90% of projected household growth in the coming decades is set to be amongst those aged 65 and over, taking the total number of homes owned by those aged 65 and over from 3.9 million today to at least five million by 2030.

Research from the Homes for Later Living Group suggests that approximately25% of the country’s 65+ population (nearly 3 million people) want to downsize. This is close to 1 million owner-occupier households. The average person under 65 moves every 12.5 years, but the equivalent figure for over 65s is 33 years because of the barriers to moving, demonstrating the need to give older people more opportunity to downsize should they wish to. These barriers include practical difficulties with moving house (due to age or illness), financial difficulties – both the cost of moving house and the cost of properties – and a lack of available, suitable homes.

The analysis also finds:

- Each person living in a home for later living enjoys a reduced risk of health challenges, contributing to fiscal savings to the NHS and social care services of approximately £3,500 per year.

- Building 30,000 more retirement housing dwellings every year for the next 10 years would generate fiscal savings across the NHS and social services of £2.1bn per year.

- On a selection of national wellbeing criteria such as happiness and life satisfaction, an average person aged 80 feels as good as someone 10 years younger after moving from mainstream housing to housing specially designed for later living.

Helping more people who wish to downsize would not only support their independent living and generate significant savings for the NHS but would also help younger families looking for a family-sized home in prime locations (such as near schools) and thus release homes suitable for first-time buyers on to the market. Research finds:

- Roughly two in every three retirement properties built releases a home suitable for a first-time buyer.

- If all the home owners over the age of 65 in England who wanted to move were able to do so, they would directly release one million properties back onto the market and free up two million spare bedrooms.

- Every ‘Homes for Later Living’ property sold generates two moves further down the housing chain, and in certain circumstances this may be more. This frees up homes at differing stages of the housing ladder for different demographics. A typical Homes for Later Living development which consists of 40 apartments therefore results in 80 additional moves further down the chain.

Solution: Require all LPAs to assess the demand for all forms and tenures of housing for older persons and include policies and a strategy for meeting this demand in local plans.

For there to be a meaningful difference made to the volume of retirement housing, it is vital that planning authorities are required to plan positively for the provision of older people’s housing and to take account of the viability challenges its delivery involves.

At present far too many planning authorities do not have adequate policies for the supply and location of older people’s housing and nor is there a consistent and positive approach to the assessment of demand for different types and tenures of such housing across authorities.

A corollary is that the viability challenges involved in delivering specialist housing for older people are not systematically taken into consideration – or understood - in the formulation of local plan policies.

In this regard, it is important to understand that specialist housing development for older people is often competing against alternative commercial uses for unallocated sites in inner urban areas, where competitors do not face the same planning obligation requirements for affordable housing and where Community Infrastructure Levy (CIL) assessments for retirement development do not take account of the schemes’ non-saleable communal areas.

Overall, the lack of positive planning for older people’s housing and the limited consideration of its commercial and viability challenges is a major reason for the current under supply of such housing.

To resolve these challenges, every Local Planning Authority (LPA) should be required to:

- Assess the demand for all forms and tenures of housing for older people and to include policies and a strategy, including land supply, for meeting this demand in its local plan. This is an essential requirement to ensure positive planning for the delivery of housing for older people. It could be introduced relatively easily through changes to the NPPF, supported by the NPPG.

- Every Local Planning Authority should indicate in its local plan areas where proposals for the development of housing for older people would be welcomed. This step would provide more confidence for developers in seeking to bring forward new schemes for older people’s housing. It could again be introduced through a change to the NPPF, supported by the NPPG.

- Local Planning Authorities should adopt policies that actively address the viability challenges which the developers of older people’s housing face. These viability challenges are well attested and need to be tackled. The requirement to adopt such policies could be another change introduced via revision of the National Planning Policy Framework (NPPF), or possibly via the inclusion of suitable provisions in the proposed national development management policies.

- Publish targets for older people’s housing and a yearly report on delivery rates.

The new Government could also consider the introduction of other measures, including:

- production of a standard methodology to determine how many homes for older persons are required to adequately meet demand each year.

- on the demand side, Stamp Duty relief for those of pension age who are downsizing would support affordability for those wishing to move and provide a wider market signal for innovation, encouraging new market entry. Overall, this would clearly enhance consumer benefit and, according to a number of studies, would also have a positive fiscal impact for the Government due to the additional moves down the housing chain and related economic activity that additional older movers would generate.

Solution: Implement the recommendations of the Older People’s Housing Taskforce when the report is published.

HBF actively supported the work of the current Government’s Taskforce on Older People’s Housing, which is considering measures to improve the supply, quality and diversity of the housing offer for older people.

With the Taskforce’s work now complete, we encourage the next Government to publish and implement the recommendations of its work as quickly as possible.

Problem: The supply of S106 Affordable Housing units is under threat

That private sector housing delivery is now responsible for providing almost 50% of all affordable homes is something that is little understood, less appreciated, by many.

In the past five years alone, almost 140,000 new affordable homes have been delivered as a result of private sector cross-subsidy with developers contributing around £7bn towards affordable housing provision, infrastructure and amenity enhancements each year.

However, the contribution developers can make to tackling the crisis in affordable housing is under threat. Home builders are reporting to HBF that they are finding it increasingly difficult to fulfil their affordable housing S106 requirements due to a lack of bids from Registered Providers (RPs).

This is despite the fact:

- 1.29 million households were on local authority social housing waiting lists as of 31 March 2023, an increase of 6% compared to 31 March 2022 and the highest it has been since 2014.

- the average monthly rent paid by tenants in the UK rose by 9% in the year to February, the highest annual increase since records began in 2015.

Frustrations with the current situation are shared by developers, RPs and LPAs alike and the issue is the result of a ‘perfect storm’ of issues including:

- Economic - In common with the broader home building industry, RPs have faced challenges due to the economic uncertainty of the past two years and particularly, high levels of inflation. Indeed, the Regulator of Social Housing (RSH) found from its survey of more than 200 large providers that cash reduced from £4.4bn to £4.2bn in the final quarter of 2023. Prior to the pandemic balances were £5.8bn with cash levels now at their lowest for 10 years.

- Rising costs - The economic challenges have occurred at a time when RPs are also required to invest heavily in building safety remediation, act on damp and mould and decarbonise and modernise existing stock. Indeed, research has found that repairs and maintenance expenditure across the sector has increased by over £1.5billion in just four years. These issues, combined with the introduction of Tenant Satisfaction Measures which focuses on matters such as the landlord’s ability to keep properties in good repair and maintain building safety, mean that any available reserves are being targeted at asset management issues rather than investment in new stock. Cost inflation is also presenting a challenge with RPs struggling particularly with maintenance contractor costs and insurance.

- Increasing cost of debt - RPs use debt (secured against stock) to fund growth and are obliged to maintain liquidity to fund at least 18 months of operation. While some is at a fixed rate, the changes in interest rates have made that debt more expensive. With the larger providers having debt running into the billions, the additional cost of servicing that debt and maintaining covenants is significant.

- Rent caps - In April 2023, the previous Government introduced a 7% cap on social housing rent for the 2023-24 financial year. While understandable, it provides another fiscal challenge for RPs at a time when the costs of maintaining and improving their existing stock are rising significantly. Some have suggested that it will result in a £3.2 billion loss in rental income for RPs. Unsurprisingly, all of these issues have an impact on the ability and willingness of RPs to invest in new housing with research finding that “RPs are planning to cut their development pipelines by 22% in the coming years”.

- Grant funding - A shift is also taking place with RPs increasingly choosing to buy land and tailor schemes towards their own requirements over purchasing S106 stock. This also enables them to access grant funding, which they cannot use on S106 units. The importance of grant funding has been summarised by Trowers and Hamlins: “grant funding is intended to assist registered providers, local authorities and other organisations (such as Almshouses or private developers) to plug a funding gap between the costs of delivering affordable housing and the level of expenditure and borrowing that can be supported by the constrained income streams deriving from it. Its injection into projects is to encourage additional delivery of affordable housing within the country.”

- Consolidation - In recent years, RPs have merged due to the aforementioned issues with the economic climate and the costs associated with building safety remediation, decarbonisation and investment in existing stock. While there are undoubtedly benefits to RPs of doing this (e.g. buying power and economies of scale), it has had a detrimental impact on local, community-based RPs who face an existential challenge with the management of smaller schemes in less dense areas becoming more expensive.

- Capacity - Due to capacity issues, many RPs, especially the larger ones, are concentrating on sites where they can deliver large numbers of affordable homes. Some commentators have suggested that “Most RPs have a minimum threshold of 20 homes, with the larger RPs not interested in delivering less than 100 homes”. As such, this presents a particular challenge for SME developers who by their very nature are focused on smaller sites which in turn generates fewer S106 affordable homes.

HBF recently conducted a survey of some of its members to better understand the extent of the current challenges. The results found that as of March 2024, there are at least 13,000 S106 units with detailed planning permission that are currently uncontracted. Most concerningly, of the units for which a completion date was provided, more than a third (37%) are due for completion in 2024/25.

Through the survey, we have been made aware of almost 40 sites that are currently delayed across the country due to uncontracted S106 units. Others are at risk of stalling as the developer is close to the threshold of how much open market housing can be constructed before S106 units are delivered.

Anecdotally, we have also heard that developers are having to reconsider their speed and direction of build to manage capital on uncontracted units. We also know that for SMEs that rely on having a contracted buyer for S106 units to access development finance, this is an insurmountable challenge without LPA flexibility.

To overcome these issues, respondents to the survey reported that S106 units are increasingly being converted to other tenures, such as First Homes or Rentplus. While these are both valuable tenures, there is a significant need for more social rented and Affordable Rent Homes.

Furthermore, in many cases, LPAs are unwilling to consider cascade arrangements as part of Section 106 agreements leaving house builders in limbo with legal obligations to provide Affordable Housing but with no active market to provide these into.

It is vital that swift action is taken to support the delivery of these much-needed homes and HBF is having regular conversations with DLUHC, Homes England, RPs, and Local Government to find and establish a solution.

Solution: Work with home builders, Registered Providers and Local Government to find a solution to the issue of uncontracted S106 units so that desperately needed Affordable Homes are not lost.

A key part of this solution could include, but not be limited to, encouraging a greater acceptance of cascade agreements by Local Planning Authorities (LPAs) which could be achieved via a Written Ministerial Statement (WMS) from the Government.

A cascade agreement allows for the affordable housing outputs to be changed – for example, if there is no interest from RPs in the proposed affordable dwellings within a certain timeframe then this can be changed to an alternative tenure or to a commuted sum in lieu of affordable housing which can be delivered elsewhere by the local authority.

Where possible, developers are working with LAs to negotiate cascade agreements but at present not all are open to their use.

Solution: Provide clarity as soon as possible on the funding and direction of the Affordable Homes Programme for 2026 and beyond and a long-term social housing rent settlement.

Homes England’s Affordable Homes Programme, which provides grant funding to support the capital costs of developing affordable housing in England, is currently set to end in 2026.

Given the reliance of RPs on grant funding and the subsequent impact it has on appetite for S106 Affordable Homes, it is vital that the next government outlines its intentions with regards to the future of the programme as soon as possible.

Similarly, the Government should also adopt a long-term approach to social housing rents which is fair to residents but also provides vital stability and certainty to housing associations. This in turn will give the sector more confidence to invest in S106 units.

Solution: Enable Homes England grant funding available for use on S106 units for a time limited period.

As outlined above, many RPs are choosing to focus solely on grant-funded units. The next government, working with Homes England, should consider whether grant funding could be made available for use on S106 units for a time-limited period.

By allowing RPs to ‘top up’ their bids with grant funding, a bit of breathing space would be created in which a longer-term solution could be sought, while also ensuring that much needed affordable new homes are not lost in the immediate to medium term.

- uid

- None

- ctype

- None

- heading

- None

- content

Increasing housing supply: Establishing a clearer and more certain policy landscape

For many decades, not enough homes have been built to meet the needs of the population. As a result of this housing shortfall, buying a home has become increasingly unaffordable, with younger generations and those on lower incomes bearing the brunt of this reality. Economic growth and job opportunities have also been constrained by limited delivery.

Problem: Housing delivery looks set to decrease further

Furthermore, as highlighted earlier in this paper, all available metrics indicate that housing delivery is set to decrease considerably in the coming months and years - threatening to make the housing crisis even more acute for many households across the country. This worsening picture is due to a combination of economic uncertainty, inflationary pressures, and policy choices taken by the previous Government.

The current outlook for housing supply in the years ahead may be dire, but this downward trend is not inevitable. Increasing housing supply is possible if the right choices are made by the new Government. Indeed, in the early-mid 2010s, the commitment of policymakers to address the long-term undersupply of housing and the willingness of ministers to challenge ‘Not in my back yard’ (NIMBY) interests brought significant results - with housing supply rising 91% from the trough in 2012-13 to a high point of almost 250,000 homes in 2019-2. Economic challenges and a changing Government approach have now undercut this progress.

However, increasing delivery will not only provide much-needed new homes but maximise the economic and social benefits of development for local communities. In the following sections, HBF is proposing several practical steps that can be taken by the next Government to boost supply.

Solution: Reverse the December 2023 changes to the National Planning Policy Framework (NPPF), with a particular focus on reinstating mandatory housing targets and the Five-Year Housing Land Supply (5YHLS).

When introduced in 2012, the NPPF helped to drive up housing supply – introducing presumptions in favour of development, and measures to speed up decision-making. The NPPF also saw councils adequately incentivised to prepare and maintain local plans.

However, some of the December 2023 changes to the NPPF have weakened these incentives, meaning that fewer planning authorities are seeking to abide by their responsibilities to plan for the number of new homes communities need.

The two changes to the NPPF that will have the greatest impact on housing supply are:

- Abolition of mandatory housing targets – The revised NPPF removes mandatory housing targets for LPAs. This means that the standard method for calculating housing need is merely an advisory starting point. Furthermore, only in exceptional circumstances, including relating to ‘the demographic characteristics of an area’, can alternative approaches to assessing housing need other than the standard method be used. This is concerning because, without clear goals in place, there is a considerable likelihood that LPAs will significantly reduce the scale of housing allocations included in local plans.

- Removal of 5YHLS requirement - LPAs with a local plan that is less than five years old will no longer need to continually demonstrate a five-year land supply. This requirement ensured that local authorities have enough available sites to meet housing requirements for the next five years, thereby acting as an important safeguard for housing supply. The 5% and 10% ‘buffers’ applied to local authorities’ 5YHLS calculations were also removed.

The weakening of these requirements will significantly constrain the delivery of new housing supply in the years ahead. Research by Lichfields carried out for HBF last year estimates that the changes to the NPPF, particularly the removal of housing targets, could see housing supply fall by 77,000 homes per year. In turn, housing supply could now fall to its lowest level since the Second World War, with the changes to the NPPF being the main contributor.

A fall in housing supply of 77,000 homes a year would not only undermine efforts to tackle the housing crisis, but could also result in a loss of £17bn of economic activity each year and threaten over 200,000 jobs in a sector which relies on extensive domestic supply chains.

It is worth noting that the recent Competition and Markets Authority (CMA) report also expressed concern over the abolition of housing targets, acknowledging that “the recent steps announced by the UK government to allow LPAs to justify not meeting housing targets in England runs contrary to the direction of travel we consider most appropriate in this area”.

Therefore, we are calling on the new Government to issue a Written Ministerial Statement (WMS) and start the process of reversing some of the revisions to the NPPF made in December 2023 as soon as possible upon taking office.

Solution: Reform the Standard Method of Housing Need

While HBF was opposed to the abolition of mandatory housing targets, it appreciates that the Standard Method could be reformed to allay some of the concerns expressed by local authorities and communities with regards to housing delivery.

Should the next Government be minded to reform, we suggest that any alternative should:

- have as its baseline the existing housing stock of an area. This figure is empirical and stable over time. Its use would avoid criticisms that have been levelled at the use of household projections (such as their datedness and volatility).

- apply to this baseline a rate by which all areas would be expected to grow their housing stock in line with a national ambition. This would ensure that the starting point for all local authorities and communities is proportionate to their existing size and that all areas contribute proportionately to new housing supply. Applying a rate by which the national housing stock should grow also ensures retention of a clear national ambition for the increase in the supply of new homes.

- be a starting point from which local assessments would be derived. Policy and guidance would make clear the parameters to be taken into account locally to inform whether in practice the level of need is higher or lower than this starting point.

An approach based on these principles would address the perception of “top-down targets” while continuing to ensure that local authorities do not duck or defer the difficult decisions needed to ensure the country’s housing needs are met. Ultimately, greater consensus on the nature of targets - and ensuring that new housing is delivered in a proportionate way - makes it more likely that these targets will be met.

Problem: There is uncertainty as how to a sustained increase in housing delivery will be achieved

There must also be a clear plan for how increases in housing delivery will be achieved. Indeed, the previous Government’s 300,000 annual target has never been achieved in part because of a lack of clarity over the steps needed to do so.

The industry has also faced considerable regulatory and political uncertainty in recent years. For instance, there have been 16 housing and planning ministers since 2010, often with shifting priorities and approaches. Another recurring theme has been delays, difficulties and uncertainty ahead of the implementation of new regulations – such as the introduction of Biodiversity Net Gain (BNG) earlier this year, or the Future Homes Standard (FHS). The industry can only be in a strong position to invest and increase housing delivery when it has certainty about the Government’s approach.

Solution: Introduce a 10-year plan for housing to tackle the housing crisis and provide longer-term certainty for the industry.

The development of a 10-year plan would be a strong foundation for efforts to increase housing supply. It would both provide industry with confidence and certainty about the broader policy and regulatory approach, while also requiring the Government to clarify the practical steps it will take to boost housing delivery.

Problem: Not enough land is being made available to develop the quantum of housing needed

In the face of an acute and worsening housing crisis, HBF considers it sensible to consider the different ways in which suitable land can be brought forward for development. Indeed, the availability of land is an ongoing concern for home builders, particularly those in the SME category.

For instance, 44% of respondents to our SME survey, run in conjunction with Close Brothers Property Finance and Travis Perkins last year, cited land availability as a major barrier to growth.

Solution: Review the Green Belt and identify areas of poor ecological value, including brownfield sites, to support the development of high quality, energy efficient new housing.

One way that this could be achieved is through a review of the Green Belt. For instance, many areas of the Green Belt are neither green nor beautiful, and previously developed sites such as petrol stations or car parks (sometimes referred to as the ‘grey belt’) offer great potential for new housing close to transport links and amenities.

As such, we consider that replacing the least aesthetic parts of the Green Belt that offer little to no ecological value with high quality, energy-efficient new homes should be a priority, while still ensuring the improvement of biodiversity and green spaces for local communities.

National planning policy has recently shifted away from this approach, with the revisions to the NPPF last December meaning that Green Belt boundaries do not need to be reviewed or altered, even if this would be the only way of meeting housing need in full. It is our view that the next Government should return to a more pragmatic approach to Green Belt policy.

The public tends to agree that this should be the approach to the Green Belt. The majority of people say that they would be supportive or not averse to more home building on areas of Green Belt land in their local area if it helped to make housing more affordable.

Respondents to a consumer survey were also considerably more supportive of building on green belt land when they were asked to consider specific types of sites, with 70% of respondents supportive in principle of homes being built on derelict buildings and 63% on disused petrol stations.

Problem: There are not enough LAs with a current Local Plan in place

Local plan preparation remains slow, with research suggesting that by the end of 2025, just 22% of LPAs will have plans that are up to date and less than five years old, compared to 33% in July 2023.

This is holding back housing supply as, according to DLUHC’s own analysis, “on average, authorities without an up-to-date Local Plan would have 14% higher housing supply if their housing supply (as a proportion of existing housing stock) were as much as those with an up-to-date plan.”

Local plans are vital in setting out a pipeline of land for future supply, clarifying how the impacts and benefits of development should be balanced in each area, and giving certainty to both the industry and local communities. Therefore, there is a clear need to ensure greater local plan coverage in England.

Solution: Introduce measures to incentivise Local Planning Authorities (LPAs) to have an up-to-date local plan in place.

While many of the measures the Government set out in its plan making consultation last year to simplify the process might lead to limited improvements, there are many other ways in which LPAs can be incentivised to keep local plans up to date. For instance:

- Ensuring that only areas with an up-to-date development plan will be in receipt of infrastructure (or equivalent) funding.

- Setting out defined timelines with set milestones for local plan preparation, backed by intervention powers.

- Considering a Green Belt designation ‘out of date’ where a local plan has not been adopted in the past five years, meaning its protection should attract reduced weight until reconfirmed by an up-to-date plan.

- Encouraging local authorities to have up-to-date local plans by recognising the existence of a local plan in the funding formula for local government grants.

- Making it more difficult for LPAs to reject planning applications if they do not have a local plan in place or if they do not have an up-to-date plan in place.

- If LPAs are to rely on a land supply of fewer than five years as an incentive for plan-making, this should apply from the point of submission not the publication of a draft.

- Allowing central government to take over the decision-making authority in a local area until a local plan is in place and as a last resort, imposing a local plan on the LPA.

- Making it a statutory requirement for LPAs to prepare a local plan.

These proposals are of varying degrees of severity, with local plan production initially being incentivised by attaching plans to infrastructure funding and local government grant formulas. The most intransigent of local authorities, however, should face central government intervention to ensure a local plan is in place (although such intervention should clearly not be a first resort).

Problem: Not all devolution deals have the necessary plan making powers

The process of devolving powers to metro mayors and Combined Authorities holds much potential and can play a significant role in boosting housing delivery. The ability to make a spatial development strategy (SDS) is the single most important tool that Mayoral Combined Authorities could use to support housing delivery in their areas. This is because the preparation of SDSs covering larger geographic areas, rather than disparate planning by over 300 English local authorities acting in isolation, is a more efficient and effective way to meet housing needs and help grow and develop the economy.

Furthermore, SDSs also ensure that any unmet housing needs arising in a specific local authority area can be delivered with the cooperation of the other constituent local authority members of the Combined Authority area - sharing this among them based on an agreed spatial pattern of distribution. This is important because many of the core cities of England are under bounded and consequently struggle to accommodate their projected housing needs and the “urban uplift” in full within their administrative boundary, such as in Birmingham.

However, few Combined Authorities have sought this power and it is confined currently to Greater Manchester, Liverpool City Region, and the West of England. Furthermore, even if the power to make a spatial strategy has been conferred, it does not follow that one will be produced, or produced with any urgency - given it is not a legal duty. Consequently, this is a power that often goes unused, as has been the case in the Liverpool City Region and the West of England Combined Authorities.

Another issue with the current spatial planning framework is that the mayor must secure the unanimous support of constituent local authorities for an SDS. This gives any one local authority a strong power of veto, especially if there is any aspect of the plan that it is uncomfortable with.

Consequently, it is very difficult to progress a spatial plan that is ambitious in terms of its development requirements if this might upset one or more local authorities, especially if it proposes a spatial pattern of development where an element of the unmet housing need in one local authority area is exported to another.

Solution: Encourage more devolution deals that confer statutory and mandatory spatial plan-making powers.

A number of measures could be taken to ensure that spatial development strategies (SDS) are adopted and become a more integral part of the country’s planning framework – thereby ensuring we can meet the housing needs of urban areas:

- Central Government should encourage more devolution deals that confer statutory spatial plan-making powers, thereby increasing the efficiency and effectiveness of the plan-making system as a whole.

- Adoption of a spatial development strategy should be statutory and mandated where these powers exist.

- Mayors could be rewarded by the Government for the production and adoption of a spatial plan with further devolved powers and funding support, including housing investment funds.

- Planning policy should be clear that local plan preparation must not be delayed while a spatial development strategy is being prepared, and support from the Government for spatial plans must be conditional upon a stiff requirement that local plan preparation continue.

- Government must review the devolution agreements to confer on mayors the same plan-making powers as those enjoyed by the Mayor of London, so that mayors do not depend on the unanimous agreement of every constituent local authority to progress a spatial plan. This will also help to accommodate the requirements of the urban uplift.

Developing a Spatial Plan for England at a central Government level – to provide confidence to industry and facilitate the delivery of new homes – would also have similar benefits to SDSs, insofar as it would into account the housing and economic needs of the country as a whole, rather than just the disparate needs of over 300 local areas that are accounted for in local plans.

- uid

- None

- ctype

- None

- heading

- None

- content

Fixing the planning process: Tackling systemic issues hindering delivery

One of the biggest challenges facing developers of all sizes across the country is how to navigate a planning process which is beset by increasing costs, delays and uncertainty.

Problem: Local Planning Authorities (LPAs) are under-resourced and this is causing delays in the planning process

There are, of course, many reasons for these delays but the pivotal one is the fact that LPAs are considerably under-resourced and understaffed. These issues are resulting in discrepancies, administrative errors, and additional delays in all aspects of the planning process. The Competition and Markets Authority’s (CMA) recent report found that only 12% of planning applications were determined within 13 weeks.

As mentioned above, this has an impact on all developers but is proving particularly challenging for SME builders whose businesses are grinding to a halt. The uncertainty and delay also have consequences for builders that rely on project-based finance.

Concerns regarding resources have coincided with a decade of falling government investment in planning departments. A 2019 analysis by the Institute for Fiscal Studies revealed that gross spend on planning and development was reduced by 42% per person between 2009/10 and 2019/20. Net spend reduced by 60%, which was the largest reduction across all areas of local government. Broadly speaking, over the past 13 years, local authorities have reduced real terms spending on planning departments by around 50% while they now receive approximately 100% more major residential planning applications.

In addition to challenges concerning capital resources, LPAs are also finding it difficult to both recruit and retain staff. Almost 6 in 10 councils (58 per cent) are struggling to recruit planning officers and 36 per cent were having problems retaining them.

As such, councils are increasingly finding themselves reliant on costly agency staff; in one LPA, 90% of staff are on temporary agency contracts. Inevitably, this is having an impact on how quickly applications are being determined and the speed at which conditions are being discharged.

While industry broadly welcomed the previous Government’s action to solidify funding for planning departments through increasing fees, those fees need to be used directly and made available very quickly. The £24 million announced in 2023 to scale up local planning capacity and the £65 million announced at the 2021spending review are a good start, but real terms funding of planning departments has fallen by more than 50% since 2010. Meanwhile, planners are now required to take more decisions and with increasing complexity of development. The Royal Town Planning Institute (RTPI) estimates that £500 million will be required over four years to address significant delays in housing policy.

Concerns regarding resources in LPAs were acknowledged recently by the CMA in its recent report. It called on the Government to “improve LPA capacity and resource by raising planning fees to a cost reflective level and ringfencing those fees”.

Solution: Reduce planning delays by putting planning services on a self-sustaining footing and ringfencing planning application fees for planning purposes.

Many developers would be amenable to paying more for planning if the service they received, the speed with which planning applications were determined and the timescales for discharge of conditions, improved rapidly.

Given housing delivery will need to play a vital role in the delivery of economic growth, it is vital that the Government works with industry, planners and local government to establish how LPAs can become self-sustaining for the long-term. Consideration should also be given to:

- making fees available to consultees for the ‘Development Team’ service.

- implementing staged payments in Planning Performance Agreements, including bonuses for over-performance and penalties for under-performance.

Problem: NIMBYism is holding back housing delivery.

Anecdotally, we are increasingly receiving reports from members that the politicisation of numerous stages of the planning process is having a significant negative impact on delivery.

It is clearly appropriate that a plan-led system should have local plans that are produced with Member involvement. However, the increasing level of political involvement in applications on allocated sites, or at the detailed stage of planning post-outline consent is not and it is proving costly and damaging to the integrity of the planning system.

Solution: Take the politics out of housing by establishing a fixed national scheme of delegation (introducing a higher threshold for reserved matters submissions to be determined by committee).

Increasing the efficiency of the planning process could be done by establishing a fixed national scheme of delegation. Essentially, this would introduce a higher threshold for reserved matters submissions to be determined by committee rather than planning officers.

At present, the threshold for when applications go before the planning committee is variable across the country. In some areas, all ‘major developments’ go before planning committee. In others, the threshold is 25 dwellings and in some, it is 200 dwellings.

Establishing a clear threshold that is consistent across the country would not only help to remove the political element from the system but also provide some much-needed certainty for developers.

It was also a suggestion put forward by the Competition and Markets Authority (CMA) in its recent report which called for the Government to formally review: “the varied LPA schemes of delegation with a view to harmonising the complex set of rules and removing the use of Planning Committees for those applications which are broadly in-line with the local plan and/or which below an agreed threshold”.

Problem: We have a plan-led planning system with too few up to date local plans in place

Local plan preparation remains slow with research suggesting that by the end of 2025, just 22 per cent of local planning authorities will have plans that are up to date and less than five years old, compared to 33 per cent in July 2023.

While many of the measures set out in the recent plan making consultation might lead to limited improvements to the planning process, it remains the case that there is no statutory requirement for LPAs to prepare one. Given the scarce resources among LPAs, reductions in local government spending and ever-rising social care costs, the situation is troubling.

Solution: Accelerate the implementation of National Development Management Policies to help speed up local plan making.

There are a number of solutions that could be implemented to speed up local plan making, including accelerating the implementation of National Development Management Policies (NDMPs).

If they perform as intended, NDMPs will make local plans faster to produce and easier to navigate.

This is because nationally important issues will be covered by NDMPS and thus provide more standardisation, leaving local plans to focus on locally-important issues.

However, there are a number of other actions the new Government could take to speed up local plan making, through a mixture of a carrot-and-stick approach. These include:

- Incentivising LPAs to have an up-to-date Local Plan in place by stating that only areas with an up-to-date development plan will be in receipt of infrastructure (or equivalent) funding, setting out defined timelines with set milestones for local plan preparation, backed by intervention powers; and where a local plan has not been adopted in the past five years a Green Belt should be considered ‘out of date’ and its protection should attract reduced weight until reconfirmed by an up-to-date plan.

- Requiring local authorities to have up-to-date local plans that meet local housing need by recognising the existence of a local plan in the funding formula for local government grants.

- LPAs should not be able to unliterally determine whether a local plan needs to be reviewed.

- Making it more difficult for LPAs to reject planning applications if they do not have a local plan in place or if they do not have an up-to-date plan in place.

- Allowing central government to take over the decision-making authority in a local area until a local plan is in place and, as a last resort, imposing a local plan on the LPA.

- Ensuring statutory consultees are involved from the beginning of the process.

- If LPAs are to rely on a land supply of fewer than five years as an incentive for plan-making, this should apply from the point of submission not the publication of a draft.

- Make it a statutory requirement for LPAs to prepare a local plan.

Problem: Slow responses from statutory consultees are further delaying the planning process

Delays in receiving responses from statutory consultees were also identified by the Competition and Markets Authority (CMA) as one of the key factors driving up the length of the planning process.

The CMA’s recent paper on planning states: “LPAs reported issues with getting statutory consultees to respond within the 21-day consultation period. Responses from statutory consultees were stated to commonly be late and, in many cases, returned well in excess of the required 21-day period. This was largely attributed to resourcing issues within the statutory consultee organisations”.

This is problematic for industry as substantive pre-application advice from LPAs and statutory consultees is vital to the formulation of any development proposals. In working up proposals, a developer will be assessing which uses could be appropriate within a given site’s developable area based upon an analysis of opportunities and constraints. It is at this crucial stage of the development process that the land value that underpins contractual arrangements between landowner and prospective developer is established.

More often than not, however, substantive preapplication advice is not provided, which means that development proposals are worked up without a complete analysis of opportunities and constraints. This can result in schemes (and the contractual arrangements behind them) being amended once a planning application has been made or in a subsequent resubmission.

Once a planning application has been made, a ‘holding response’ from consultees is increasingly being issued, and in some cases, it is taking statutory consultees three to six months to respond fully. This further contributes to the length of time it takes for planning applications to be processed and, once approved, for development to start on site.

Solution: Rationalise the list of statutory consultees, seek greater involvement from them in the scoping of planning application material and ensure effective monitoring and enforcement of deadlines for their responses.

Tackling these challenges will require a number of solutions, including:

- Rationalising the list of statutory consultees and seek greater involvement from them in the scoping of planning application material.

- If an applicant has consulted the consultee at pre-application stage and there have been no substantial changes to the submitted application proposals, then substantive preapplication responses should be a material consideration in the determination of a planning application for 12 months.

- Holding objections should not be able to delay the determination of a planning application.

- Enabling effective monitoring and enforcement of deadlines for statutory consultees by:

- giving clear and advance notice to statutory consultees of the change in approach;

- issuing regular reminders to statutory consultees during the 21-day period and a final notice close to the end of the 21-day period; and

- issuing notices of deemed consent upon expiry of the deadline.

Problem: The current system of developer contributions is not fit for purpose

Local authorities require developers to make financial contributions as part of the process of granting planning permission. The purpose of these contributions is to mitigate the potential impact of development on local communities and to fund social infrastructure such as extra school facilities, health provision, open spaces, affordable housing, and highways.

Under the current arrangements, developers make contributions worth around £7 billion per annum in total. The majority of these contributions go towards affordable housing provision, and this has increasingly been the case over time.

Developer contributions are collected in three ways: as part of Section 106 (S106) agreements/planning obligations, the Community Infrastructure Levy (CIL), and highways contributions (Section 278 and Section 38 agreements).

A number of steps can be taken to improve the current framework for developer contributions.

- Reform S106/CIL by ensuring wider use of standard template agreements as a basis for negotiation to ensure consistency across the country and mitigate delays.

- Support SME developers by introducing a presumption in favour of development on small sites, up to 25 homes, on brownfield land.

Solution: Abandon plans to introduce an Infrastructure Levy (IL) and reform S106/CIL by ensuring wider use of standard template agreements as a basis for negotiation to ensure consistency across the country and mitigate delays.

The current Government has proposed a new Infrastructure Levy (IL), the framework for which is included in the Levelling Up and Regeneration Act (LURA). The new levy proposes to replace the current system of developer contributions (S106/CIL) with a mandatory, streamlined and locally-determined levy.

The key principles of the proposed IL are:

- The levy will be charged on the value of a property at completion per square metre and applied above a minimum threshold.

- Levy rates and minimum thresholds will be set and collected locally, and local authorities will be able to set different rates within their area.

- Levy charging schedules will be published and make the expected value of a contribution clear up-front.

However, HBF – alongside housing associations, charities and some local authorities – have criticised the proposed Levy. The main concerns about the proposed IL are:

- At a time of ongoing economic uncertainty, an increasing burden of regulation, and ongoing delays in the planning process, a costly and time-consuming overhaul of the developer contribution system could be counterproductive and further delay the delivery of new housing.

- Since the proposals will operate as a fixed charge it will be impossible to set an IL rate (or set of rates) that will not either render otherwise deliverable sites unviable or result in a significant volume of sites paying less IL than they could deliver. In turn, the Infrastructure Levy system could also see a lower level of delivery of affordable housing being delivered than under the current system.

- The number of rates underpinning the levy could feasibly run into the dozens - the proposed levy would require a triangulation of charging rates to account for different uses of different scales (e.g. building heights), different areas of an authority, existing and benchmark land values, and different costs, revenues and margins.

However, that is not to say that there are no issues with the existing system, particularly concerning the process of negotiating and delivering on S106 Agreements. For instance, there are often avoidable delays in the negotiation process as each agreement is drawn up from scratch, as well as opaqueness and uncertainty over how and when S106 funds are collated and spent.

Measures to mitigate delays in negotiations could include:

- Increasing permanent staff levels in Local Planning Authorities, thereby reducing reliance on locum solicitors to negotiate S106 agreements.

- The wider use of standard template agreements as a basis for negotiation to ensure consistency across the country and mitigate delays.

S106 contributions that are made to developers are also often held unspent by local authorities for extended periods of time. In total, HBF estimates that around £2.8 billion is held unspent in local authority bank accounts, including £567 million allocated for Affordable Housing.

While S106 funds inevitably take time to be spent, this often takes longer than expected due to a lack of capacity within local authorities, and a lack of effective monitoring of funds by councils. In turn, these delays are undermining support for new development as the infrastructure needed alongside new housing is not being immediately provided for local communities.

Measures to ensure developer contributions are spent in a timely way could include:

- Compelling local authorities to publish an easily digestible annual summary on their website of how money from developers is being spent and why it is not being spent.

- Introducing new provisions in legislation. Provisions already exist preventing Community Infrastructure Levy (CIL) from being spent on anything other than infrastructure, but there are no mechanisms for ensuring that revenue raised through CIL is transferred to county councils, or that any of the revenue raised through CIL/S106 is actually spent at all.

- uid

- None

- ctype

- None

- heading

- None

- content

Unblocking the housing pipeline: Finding a resolution to nutrient neutrality

Over the past five years, the construction of 160,000 new homes across a quarter of the country has been blocked due to interventions from Natural England over concerns about high nitrate and phosphate levels in England’s waterways. While it is widely acknowledged that the contribution of the occupants of new homes to this issue is negligible, it is only the home building industry that has seen an embargo imposed.

Problem: Housing delivery remains blocked by nutrient neutrality mitigation measures

Following a European Court of Justice ruling in 2018 known subsequently as ‘Dutch N’, in 2019 Natural England revised its guidance to local authorities in the Solent area that all new development involving overnight stays should be subject to an assessment under the Habitats Regulations to ensure that the proposal is ‘nutrient neutral’, i.e., that the volume of nitrates potentially entering the water system as a result of a new development must be offset by the removal of an equivalent amount. This was a policy intervention that could not have been foreseen, driven by an agency not directly involved in housing or planning.

In the years since, the restrictions have spread from the Solent and now cover 74 local authorities with an estimated 160,000 new homes held up in the planning process - ranging from sites with an allocation in local plans to those with full planning permission, and even some sites where construction has commenced but occupation of homes is prohibited.

Nitrates and phosphates enter waterways primarily from agricultural runoff, but also through sewage as a result of insufficient wastewater infrastructure. Research undertaken by Brookbanks on behalf of HBF finds that agriculture accounts for 70% of the nitrogen released into our rivers, and 25% of phosphates. In contrast, the occupancy of new homes accounted for just 0.29% of total nitrogen emissions each year and 0.73% of total phosphorus, based on an assumption that each new home will increase the local population by 2.4 people – the assumption that Natural England uses. However, with the actual average additional occupancy rate of 1.65, the proportion of nutrients accounted for from wastewater from net additional population falls to 0.2% for nitrogen and 0.5% for phosphorus – less than 1% of total nutrient pollution.

The research also finds that each dairy cow produces nitrogen equivalent to 29 homes while each sheep is responsible for the same amount of nitrogen as three family homes.

Despite this, while Natural England continues to impose a ban on new housing, farmers are granted licenses to use additional nutrient rich fertilisers, over and above the agreed European limits. This is resulting in hundreds of thousands of additional kilograms of nitrogen spread on agricultural land in Nitrate Vulnerable Zones (NVZs). In addition, planning permissions for new farming facilities continue to be granted, including for highly polluting Intensive Poultry Units to accommodate tens of thousands of hens, the result of which will see nutrient pollution increase at much greater levels than sustained levels of house building would ever produce.